What Is Tokenization and How Does It Work

Introduction

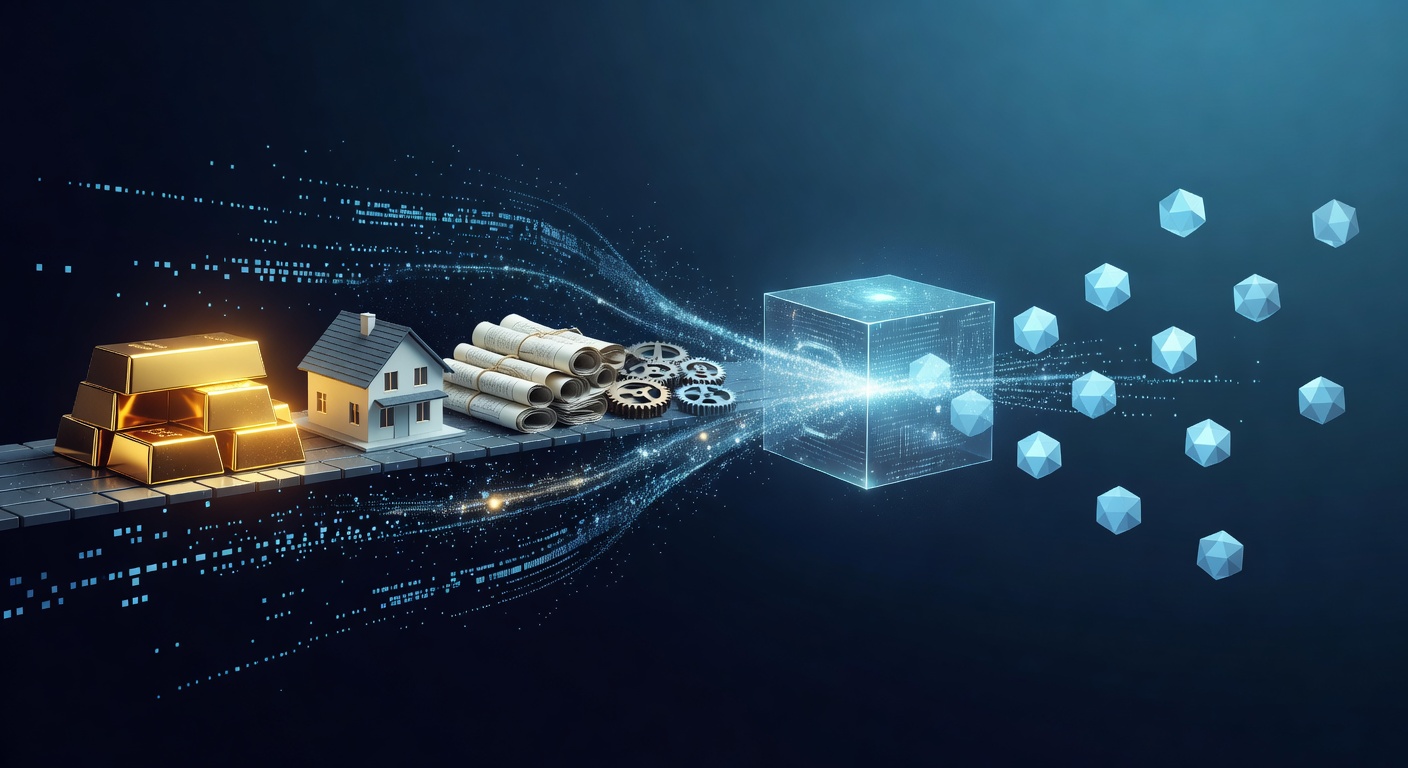

Tokenization in crypto and finance is the process of turning real-world assets or digital rights into blockchain-based tokens. Instead of relying only on ledgers and paperwork, ownership and value are represented as units that can be tracked, transferred, and verified on a network.

At its core, tokenization “wraps” an asset—such as cash, stocks, real estate, or carbon credits—into a digital form. These tokens can represent ownership, access, or claims, depending on the structure and rules behind the asset.

In crypto, tokenization often means creating new tokens on a blockchain using standards like ERC-20 or ERC-721. In traditional finance, it typically refers to issuing regulated tokenized securities or tokenizing funds to improve efficiency and access.

How it works usually involves two key steps: creating a token and linking it to a real asset or legal claim. This link may be managed through smart contracts on-chain, trusted custodians, escrow arrangements, or hybrid systems that combine software automation with legal documentation.

Once issued, tokens can move through blockchain transactions much faster than many conventional processes. Ownership updates become transparent and auditable, and certain actions—like settlement or dividend distribution—can be automated if the setup supports it.

Tokenization also changes how value is exchanged. Instead of waiting for traditional clearing and settlement cycles, participants may be able to transfer tokens instantly and interact with the asset within compliant platforms.

This article breaks down what tokenization means in practice, how tokens are issued and governed, and what makes the technology useful for both crypto-native projects and emerging finance applications.

What Is Tokenization in Crypto and Finance?

Tokenization is the process of representing real-world value—such as cash, bonds, real estate, or even company shares—by issuing digital tokens on a blockchain (or another distributed ledger). In simple terms, the question of what is tokenization becomes: how can we turn an asset into a programmable unit that can be transferred, tracked, and potentially shared among multiple participants?

In finance, this idea is often described as asset tokenization. The underlying asset may be held in custody or represented through legal agreements, while the token acts as the on-chain interface for ownership, rights, or claims. As a result, token holders can transfer value without relying entirely on traditional intermediaries like transfer agents or certain clearing mechanisms.

In tokenization crypto ecosystems, blockchain smart contracts play a central role. They can define who is allowed to mint or burn tokens, how ownership is recorded, and what restrictions apply (for example, KYC/AML requirements or investor eligibility). Moreover, smart contracts enable automation of lifecycle events, such as distributing dividends, updating corporate actions, or triggering settlement logic when predefined conditions are met.

To understand how it works, consider the typical flow. First, an issuer selects an asset and determines the token’s legal and economic structure. Next, the token is created with metadata that maps it to the real asset and its rules. Then, control layers are established: custody arrangements, compliance checks, and on-chain permissions are designed to ensure that the token’s representation matches the off-chain reality.

After issuance, tokens can be traded on supported venues or transferred peer-to-peer. However, the transferability of tokenized assets depends on the system design—some tokens are fully liquid, while others are restricted to certain counterparties. That brings an important transition: while blockchain improves transparency and programmability, the system is only as robust as its trust model, including smart contract security, custody practices, and the accuracy of the token-to-asset linkage.

Therefore, tokenization should be viewed not only as a technical mechanism, but also as a coordination of legal, operational, and cryptographic components. When these pieces align, tokenized finance can increase efficiency and access; when they do not, technical and compliance risks may emerge.

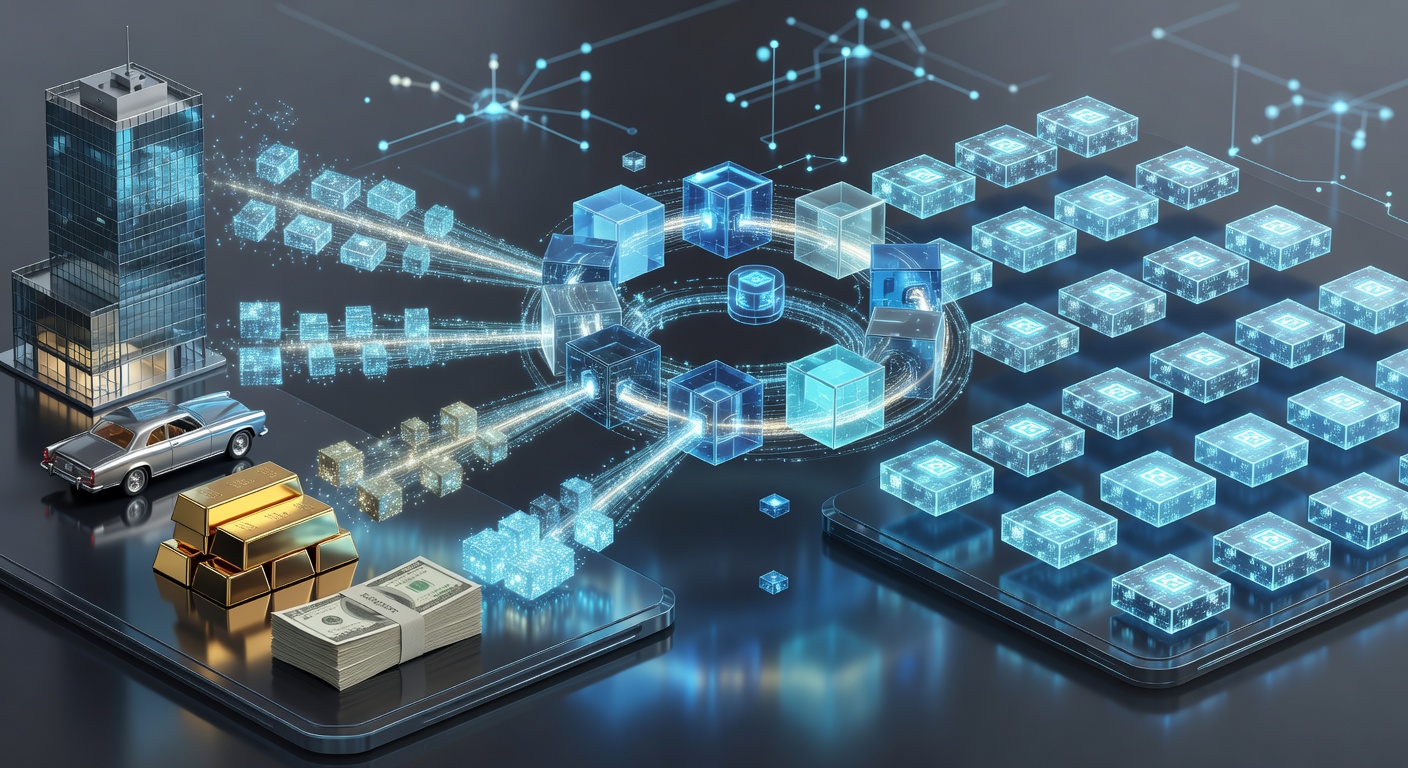

What Asset Types Can Become Tokens?

Once you understand what is tokenization in practice, the next question is naturally: which things can be represented as tokens? In tokenization crypto, the key idea is that almost any asset with definable ownership, rules, and cash flows can be mapped into a digital representation on-chain. However, the suitability depends less on the asset’s “digitalness” and more on how clearly its rights and settlement can be expressed.

To begin with, many token systems start with fungible financial assets. These include stablecoins, tokenized deposits, treasury instruments, and tokenized debt. Because such assets are interchangeable in standard units, they fit well with smart contracts that track balances, automate transfers, and enforce compliance rules. This is one of the most common implementations of asset tokenization, since their economics are relatively straightforward.

In contrast, non-fungible and semi-fungible assets are also widely tokenized. Real estate shares, invoices, carbon credits, and collectible assets can be tokenized as unique or limited-supply tokens. Here, token metadata and token-specific rules become crucial, because each unit may represent different properties, valuations, or redemption conditions. As a result, the system often needs more sophisticated data management than standard payment tokens.

Next, tokenization extends beyond traditional finance into physical-world assets. For example, artwork, commodities, and fine wines can be represented by tokens that correspond to custody arrangements or certification records. In these cases, the blockchain does not replace legal ownership by itself; rather, token holders rely on off-chain mechanisms such as custody, audits, and transfer agreements. Therefore, clear governance and auditability are essential to prevent mismatch between on-chain tokens and off-chain reality.

Another category involves contract-based and rights-based instruments. Participation rights, royalties, revenue shares, and tokenized subscription rights can be encoded so that payments, distributions, and expiries follow deterministic logic. This can reduce operational friction, but it also shifts attention toward smart contract correctness and dispute handling—especially when underlying agreements are complex.

Finally, the “what can be tokenized” question also includes intangible assets, such as access rights, identity attributes, or permissions—provided the system has a verifiable way to define and enforce those rights. Taken together, these examples show that tokenization is less about the asset’s form and more about the ability to model ownership, transfer, and settlement rules reliably.

How Tokens Represent Value Through On-Chain Rights

To understand what is tokenization, it helps to move beyond the idea that tokens are “just numbers.” In practice, a crypto token is a programmable unit that can represent rights—claims on cash flows, ownership, governance, or access—defined in code and enforced by the blockchain’s execution rules.

First, consider the core mechanism: when asset tokenization is used, a real-world or financial asset (such as a bond, invoice, or share) is mapped to an on-chain representation. That representation typically takes the form of a token whose ledger entries correspond to ownership or participation. As a result, value is not merely carried by the token; it is anchored to a defined legal and technical relationship that the system can track transparently.

Next, these rights must be made explicit. Many projects encode token behavior directly into smart contracts—transfer permissions, redemption schedules, interest distributions, or voting power. For example, a token may grant holders the right to redeem it for underlying collateral, or to receive periodic payouts funded by an escrowed treasury. Consequently, the token becomes a portable receipt for specific entitlements rather than a vague “proxy” for value.

Then there is the question of how those rights are enforced. On-chain rules provide verifiable execution: when conditions are met (a settlement date arrives, collateral is sufficient, a vote passes), the contract can automatically perform the corresponding actions. This reduces reliance on manual processes and creates an auditable trail of state changes, which is crucial for trust in tokenization crypto systems.

However, tokenization also introduces responsibility at the design and integration layer. Since the token’s meaning depends on the smart contract logic and any off-chain agreements, mismatches between legal intent and technical implementation can create risk. Therefore, robust systems define clear mappings between token units and the underlying rights, including issuance rules, redemption mechanics, and custody or settlement procedures.

In summary, how tokens represent value through on-chain rights is best seen as a combination of (1) a standardized ledger for accounting and transfer, and (2) smart-contract logic that implements and enforces entitlement rules. When done correctly, tokenization turns complex financial rights into efficient, verifiable, and interoperable primitives for modern finance.

What Role Smart Contracts Play in Token Issuance and Transfers

Smart contracts are central to how tokenization functions in practice. After defining what is tokenization and recognizing how tokenized instruments can represent real-world value, the next step is to understand how those representations get issued and moved safely. In tokenization crypto systems, the “token” is not just a balance entry—it is governed by programmable rules executed on-chain.

At issuance time, a smart contract defines the token’s core parameters: total supply, minting permissions, metadata, and—when applicable—compliance logic. This is where asset tokenization becomes concrete. For example, an issuer may encode rules such as “only the admin can mint,” or “tokens can only be minted to addresses that pass a verification check.” In more advanced designs, contracts can incorporate vesting schedules, royalties, or transfer restrictions tied to regulatory requirements.

Once issued, transfers are also handled by smart contracts rather than by a centralized database. Typically, when a user sends tokens, the contract validates whether the transfer is allowed and then updates internal ledger states atomically. This process reduces common failure modes, such as partial execution or inconsistent accounting. Additionally, smart contracts can enforce permissions for trading, pause transfers during incidents, or restrict transfers to approved counterparties.

To see why this matters, consider the difference between an off-chain IOU system and an on-chain token. In an off-chain model, trust is required to ensure balances are accurate and rules are followed. In contrast, with smart contracts, the validation and state transitions occur deterministically on-chain. As a result, anyone can independently verify token balances and transfer history through public logs, which strengthens transparency.

However, these benefits also make security critical. Because smart contracts are immutable after deployment (or difficult to change safely), flaws in the issuance or transfer logic can create systemic risks. Practical risk mitigation therefore includes thorough testing, formal verification where feasible, and independent audits focused on authorization checks, arithmetic correctness, and edge cases in transfer hooks and upgrade mechanisms.

In summary, smart contracts provide the operational “engine” for token issuance and transfers. They translate the concept of tokenization into enforceable, verifiable rules—making tokenized assets programmable, composable, and trackable, while also requiring careful security engineering to prevent vulnerabilities.

How Token Standards Affect Interoperability and Risk

After clarifying what tokenization is and how tokenized assets can be represented on-chain, the next key step is understanding that not all tokens behave the same way. In practice, token standards define how tokens are issued, transferred, approved, and tracked. Therefore, when systems use different standards, integration becomes harder and interoperability may suffer.

To see why this matters, consider what is tokenization in the real world: an investment, invoice, or real-world asset is “wrapped” into a digital token. That token must follow a set of rules so wallets, exchanges, custody services, and smart contracts can recognize it. When a protocol chooses one standard and another ecosystem chooses a different one, bridges or adapters are often required. This is common in tokenization crypto ecosystems, where tokenized representations proliferate across multiple chains and applications.

Common standards (for example, Ethereum-based fungible and non-fungible interfaces) typically improve compatibility within the same family of tools. However, they do not automatically guarantee cross-chain behavior. A token contract may technically adhere to a standard on one network but still be incompatible with how another network handles metadata, permissions, royalties, or token lifecycle events. Consequently, interoperability becomes an engineering effort rather than a “free” property.

Beyond integration, standards also influence security risk. Smart contract platforms often assume specific behaviors when interacting with tokens—such as consistent balance accounting or predictable transfer semantics. If a token deviates from expectations (for example, by using non-standard return values or custom transfer logic), integrations can break or become vulnerable. Moreover, some standards encourage extension mechanisms—like transfer hooks—which can introduce reentrancy surfaces if consuming contracts are not carefully designed.

Additionally, asset tokenization frequently involves permissions and compliance layers. Token standards may interact with allowlists, role-based access control, or upgradeable contracts. If those mechanisms are implemented inconsistently, users may face transfer failures, stuck balances, or unintended operator rights. Over time, these “edge cases” accumulate into operational and security risk.

In summary, token standards are the connective tissue of token ecosystems: they enable interoperability, but they also set assumptions that integrators must respect. As tokenization spreads across chains and platforms, aligning standards—and validating their real-world behaviors—becomes essential to reduce both technical friction and systemic risk.

How Liquidity, Settlement, and Compliance Work Together

In tokenization crypto, converting real-world value into on-chain tokens is only part of the story. Just as important are the mechanisms that make those tokens usable: liquidity, settlement, and compliance. When these three elements work together, tokenized assets can move from “digital representation” to “tradable and redeemable instruments” in practical markets.

To begin with, liquidity determines whether tokenized products can be bought and sold efficiently without excessive price slippage. In practice, liquidity emerges from market structure (exchanges, liquidity pools, market makers) and from how token ownership maps to underlying rights. For example, if an asset tokenization platform can quickly match buy and sell orders and enforce transfer rules, traders gain confidence—and narrower spreads usually follow. Conversely, thin liquidity can make even well-designed assets economically fragile.

Next, settlement is the process that finalizes transactions and ensures that transfers are irreversible once confirmed. In a blockchain-based system, settlement typically occurs via smart contracts that atomically update balances and record ownership. This reduces reliance on manual reconciliation and long settlement windows that traditional finance often suffers from (e.g., multi-day clearing). As a result, settlement finality can improve capital efficiency, because participants spend less time waiting for “paper-based” confirmation.

However, settlement alone does not guarantee safety or regulatory alignment. Therefore, compliance must be integrated into the asset lifecycle. In many implementations of what is tokenization, token transfers are not purely “send and receive” operations; they may require restrictions based on jurisdiction, investor eligibility, or sanctioned entities. Compliance can be enforced using allowlists, permissioned token contracts, whitelisting modules, or transfer-validation logic. This is especially relevant for asset tokenization where the token represents a claim on regulated rights, such as securities, funds, or debt instruments.

When you connect these layers, the flow becomes clear. Liquidity providers need predictable settlement, settlement requires reliable state transitions and governance, and compliance must be applied without breaking the market’s ability to trade. A well-architected tokenization system aligns smart contract rules with regulatory requirements while still enabling fast execution for traders. This balance is where successful tokenized markets differentiate from experiments: they are not only tokenized, but also operationally and legally executable.

Ultimately, understanding how liquidity, settlement, and compliance interact helps you evaluate risk. If any component is misaligned—slow settlement, fragmented liquidity, or overly rigid compliance enforcement—trading and redemption can fail at the worst possible time.

What Technical and Regulatory Risks Come With Tokenization

Once you understand how tokenization works—typically by representing real-world rights or digital assets as tokens on a blockchain—it becomes essential to evaluate the risks that accompany this approach. In practice, “what is tokenization” is not just a technical question. It also introduces security, compliance, and operational challenges that can be underestimated when teams focus only on innovation.

On the technical side, the first major risk is smart contract correctness. In tokenization crypto systems, ownership rules, transfer restrictions, and redemption logic are often enforced by on-chain code. If that code has vulnerabilities—such as flawed access control, unsafe upgrade mechanisms, or incorrect accounting—token holders may face loss of funds, broken redemption paths, or unintended minting. Even when the contract is audited, upgrades, oracle integrations, and third-party dependencies can reintroduce attack surfaces over time.

Next, consider custody and key management. Tokenized assets are only as secure as the private keys controlling them. If a platform uses custodial wallets, it inherits the risk profile of a traditional financial custodian, including operational failures and breach events. If it relies on self-custody, user errors (lost keys, misconfigured wallets, phishing) become a frequent operational hazard. Therefore, asset tokenization systems must carefully define who can move tokens, who can freeze or reverse transactions, and what happens in emergency scenarios.

Then there is the “data layer” risk: blockchain finality does not automatically guarantee real-world validity. If token issuance depends on off-chain records—such as identity verification, KYC status, collateral valuations, or legal ownership—mismatches between on-chain data and off-chain reality can occur. Oracle manipulation, inaccurate valuation feeds, or delayed updates can cause pricing errors, under-collateralization, or disputes about legitimate ownership.

While technical safeguards are necessary, regulatory risk is often the decisive factor. Many jurisdictions treat tokenized instruments as securities, derivatives, commodities, or e-money depending on their economic function, promotion, and distribution. As a result, teams must assess whether their tokens trigger licensing, prospectus requirements, trading venue rules, or ongoing reporting obligations. Cross-border issuance further complicates compliance due to differing interpretations of similar token structures.

Finally, liquidity and governance risks can amplify both technical and regulatory pressures. If compliance constraints prevent transfers or exchanges, token liquidity may fragment. Meanwhile, governance mechanisms (including role-based permissions and settlement processes) must be designed to prevent misuse and ensure continuity during disputes or insolvency events.

In summary, tokenization can improve access and automation, but it also requires rigorous security engineering and proactive legal compliance to reduce the likelihood of high-impact failure modes.

Frequently Asked Questions

How does tokenization differ from issuing a traditional security?

Tokenization turns rights into digital units that can move on-chain. A traditional security is recorded and transferred through legacy registries and intermediaries. In practice, many tokenized securities still require legal documentation and compliance controls—on-chain just changes settlement and transfer mechanics.

What is the difference between tokenization “on-chain” and “off-chain” custody of value?

On-chain custody means the underlying rights or assets are represented and governed by smart contracts (or tokenized vault logic). Off-chain custody means the real-world asset sits with a custodian or legal entity, while tokens represent claims to that off-chain position. The second model introduces a trust and operational dependency that smart contracts alone can’t remove.

If tokens are transferable, how are ownership and redemption handled for tokenized real-world assets?

Ownership is tracked by the token ledger (wallet balances/receipts), but redemption depends on the asset’s governance model. Typically, a redemption request burns or locks tokens and triggers an off-chain workflow to release the underlying asset or cash. That workflow can involve KYC/AML, whitelist/blacklist checks, and time delays—so the on-chain transfer isn’t always equivalent to immediate settlement.

What technical failure modes should I watch for in tokenization systems?

Common issues include smart contract upgrade mistakes, flawed access control, and incorrect accounting between on-chain and off-chain components. For bridged assets, a bridge failure can break the 1:1 mapping between wrapped tokens and their backing. Even without “hacks,” mismatched decimals, rounding, or role permissions can create long-tail losses and settlement disputes.

Conclusion

Tokenization is the process of converting sensitive data into non-sensitive tokens that can be safely used, stored, and processed without exposing the original information. It works by replacing each piece of data (like a credit card number or personal identifier) with a unique token generated by a tokenization system. When needed, authorized systems can use the token to retrieve or map back to the original data through a secure token vault using strict access controls. By separating data from its usable form and limiting direct exposure, tokenization reduces the risk of breaches and helps organizations comply with privacy and security requirements while still enabling essential business operations.